Blank North Carolina 91C PDF Form

Blank North Carolina 91C PDF Form

When facing financial turmoil, many North Carolinians find themselves navigating the complexities of the bankruptcy process, seeking relief and a fresh start. Among the critical steps in this journey is completing the North Carolina 91C form, an official document utilized in the United States Bankruptcy Court for the Middle District of North Carolina. This form serves a pivotal role for debtors declaring bankruptcy, as it allows them to claim property exemptions under specific statutes. The document meticulously lists various assets that a debtor can declare as exempt, ranging from the debtor’s residence or burial plot to personal property needed for household or personal purposes, motor vehicles, tools of trade, and even retirement benefits, among other items. Importantly, the form is designed to protect certain assets from being seized or sold off to pay creditors, thereby providing a safety net that ensures debtors are not left destitute post-bankruptcy. It outlines the applicable exemptions as per 11 U.S.C. '522(b)(3)(A), (B), and (C), the Laws of the State of North Carolina, and non-bankruptcy federal law, making it essential for debtors to understand and accurately claim their rightful exemptions. With provisions for both federal and state-specific exemptions, the 91C form reflects a nuanced approach, accommodating a range of personal circumstances, such as age and marital status, further compounded by stipulations like the recent purchase rule that disallows certain exemptions for newly acquired properties.

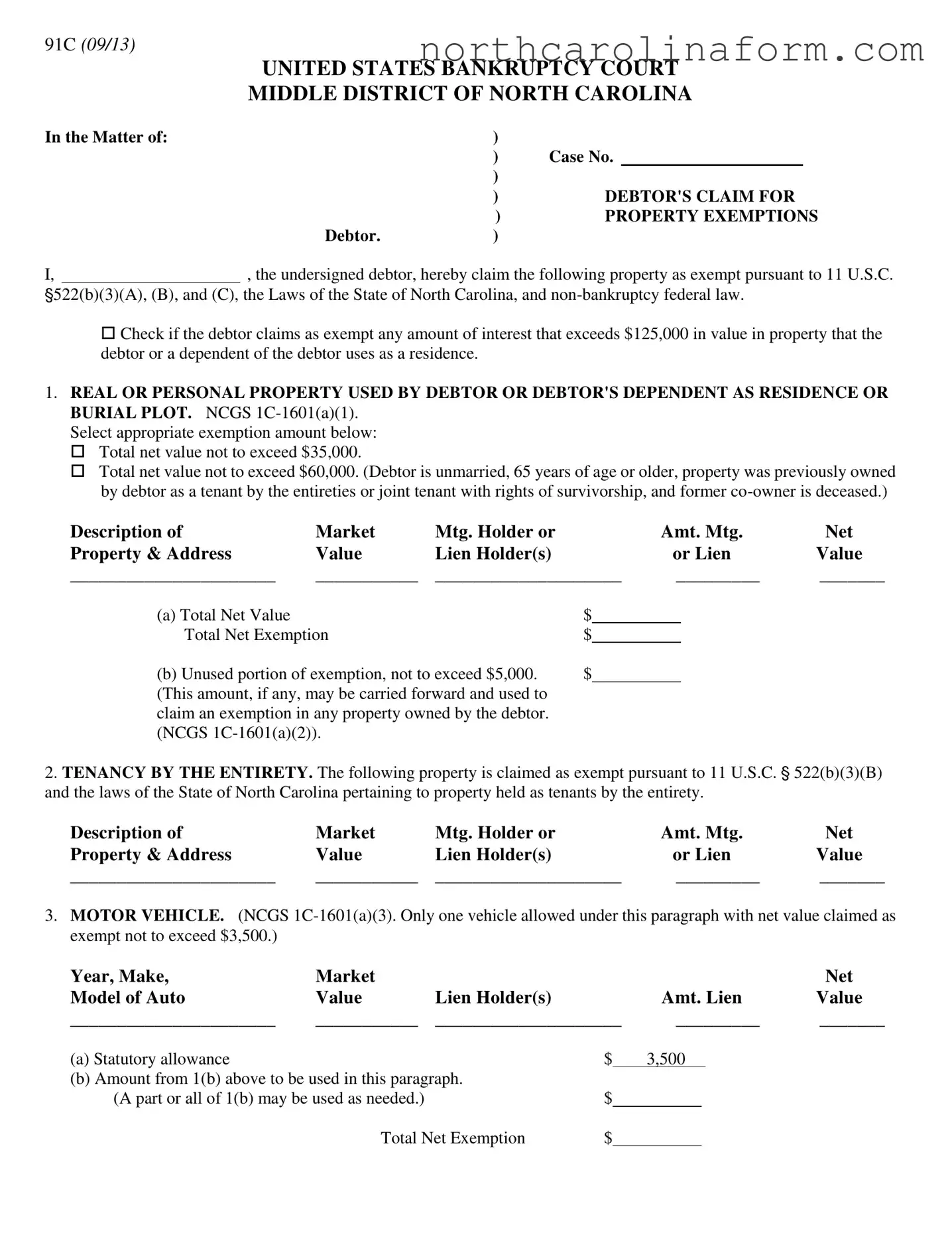

91C (09/13)

UNITED STATES BANKRUPTCY COURT

MIDDLE DISTRICT OF NORTH CAROLINA

In the Matter of: |

|

) |

|

|

|

|

|

|

|

) |

Case No. |

||

|

|

|

) |

|

|

|

|

|

|

) |

DEBTOR'S CLAIM FOR |

||

|

|

|

) |

PROPERTY EXEMPTIONS |

||

|

|

Debtor. |

) |

|

|

|

I, |

|

, the undersigned debtor, hereby claim the following property as exempt pursuant to 11 U.S.C. |

||||

'522(b)(3)(A), (B), and (C), the Laws of the State of North Carolina, and

Check if the debtor claims as exempt any amount of interest that exceeds $125,000 in value in property that the debtor or a dependent of the debtor uses as a residence.

1.REAL OR PERSONAL PROPERTY USED BY DEBTOR OR DEBTOR'S DEPENDENT AS RESIDENCE OR BURIAL PLOT. NCGS

Select appropriate exemption amount below:

Total net value not to exceed $35,000.

Total net value not to exceed $60,000. (Debtor is unmarried, 65 years of age or older, property was previously owned by debtor as a tenant by the entireties or joint tenant with rights of survivorship, and former

Description of |

Market |

Mtg. Holder or |

Amt. Mtg. |

Net |

Property & Address |

Value |

Lien Holder(s) |

or Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

(a) Total Net Value |

$ |

|

|

Total Net Exemption |

$ |

|

|

(b) Unused portion of exemption, not to exceed $5,000. |

$ |

|

|

(This amount, if any, may be carried forward and used to |

|

|

|

claim an exemption in any property owned by the debtor. |

|

|

|

(NCGS |

|

|

|

2.TENANCY BY THE ENTIRETY. The following property is claimed as exempt pursuant to 11 U.S.C. ' 522(b)(3)(B) and the laws of the State of North Carolina pertaining to property held as tenants by the entirety.

Description of |

Market |

Mtg. Holder or |

Amt. Mtg. |

Net |

Property & Address |

Value |

Lien Holder(s) |

or Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

3.MOTOR VEHICLE. (NCGS

Year, Make, |

Market |

|

|

|

|

|

|

Net |

Model of Auto |

Value |

Lien Holder(s) |

|

|

Amt. Lien |

Value |

||

______________________ |

___________ |

____________________ |

_________ |

_______ |

||||

(a) Statutory allowance |

|

|

$ |

|

3,500 |

|

|

|

(b) Amount from 1(b) above to be used in this paragraph. |

|

|

|

|

|

|

||

(A part or all of 1(b) may be used as needed.) |

|

$ |

|

|

|

|

|

|

|

Total Net Exemption |

$ |

|

|

|

|

|

|

91C (09/13)

4.TOOLS OF TRADE, IMPLEMENTS, OR PROFESSIONAL BOOKS. (NCGS

|

Market |

|

|

|

|

Net |

Description |

Value |

Lien Holder(s) |

|

|

Amt. Lien |

Value |

______________________ |

___________ |

____________________ |

|

_________ |

_______ |

|

______________________ |

___________ |

____________________ |

|

_________ |

_______ |

|

(a) Statutory allowance |

|

$ |

2,000 |

|

|

|

(b) Amount from 1(b) above to be used in this paragraph. |

|

|

|

|

||

(A part or all of 1 (b) may be used as needed.) |

$ |

|

|

|

|

|

Total Net Exemption $

5.PERSONAL PROPERTY USED FOR HOUSEHOLD OR PERSONAL PURPOSES NEEDED BY DEBTOR OR DEBTOR'S DEPENDENTS. (NCGS

|

|

Market |

|

|

|

|

|

|

|

Net |

|

Description |

|

Value |

Lien Holder(s) |

|

Amt. Lien |

Value |

|||||

Clothing & Personal |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Kitchen Appliances |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Stove |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Refrigerator |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Freezer |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Washing Machine |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Dryer |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

China |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Silver |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Jewelry |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Living Room Furniture |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Den Furniture |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Bedroom Furniture |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Dining Room Furniture |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Lawn Furniture |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Television |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

( ) Stereo ( ) Radio |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Musical Instruments |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

( ) Piano ( ) Organ |

___________ |

____________________ |

|

_________ |

_______ |

||||||

Air Conditioner |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Paintings & Art |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Lawn Mower |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Yard Tools |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Crops |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Animals |

|

___________ |

____________________ |

|

_________ |

_______ |

|||||

Other ( |

) |

___________ |

____________________ |

|

_________ |

_______ |

|||||

|

|

|

|

|

Total Net Value $ |

|

|||||

(a) Statutory allowance for debtor |

|

|

|

|

$ |

5,000 |

|

|

|

|

|

(b) Statutory allowance for debtor's dependents: |

|

|

dependents |

|

|

|

|

|

|

||

at $1,000 each (not to exceed $4,000 total for dependents) |

$ |

|

|

|

|

|

|||||

91C (09/13)

(c) Amount from 1(b) above to be used in this paragraph. |

|

|

|

|

|

|

|

|

|

||

(A part or all of 1 (b) may be used as needed.) |

$ |

|

|

|

|

|

|

||||

|

|

|

Total Net Exemption $ |

|

|

||||||

6. LIFE INSURANCE. (As provided in Article X, Section 5 of North Carolina Constitution.) |

|||||||||||

Name of Insurance Company |

|

|

|

Policy No. |

|

||||||

Name of Insured |

|

|

|

Policy Date |

|

||||||

Name of Beneficiary

7.PROFESSIONALLY PRESCRIBED HEALTH AIDS (FOR DEBTOR OR DEBTOR'S DEPENDENTS). (NCGS

Description:

__________________________________________________________________________________

8.DEBTOR'S RIGHT TO RECEIVE FOLLOWING COMPENSATION: (NCGS

A. |

$ |

|

Compensation for personal injury to debtor or to person whom debtor was dependent for support. |

B. |

$ |

|

Compensation for death of person of whom debtor was dependent for support. |

C. |

$ __________ |

Compensation from private disability policies or annuities. |

|

9.INDIVIDUAL RETIREMENT PLANS AS DEFINED IN THE INTERNAL REVENUE CODE AND ANY PLAN TREATED IN THE SAME MANNER AS AN INDIVIDUAL RETIREMENT PLAN UNDER THE INTERNAL REVENUE CODE (NCGS

DEFINED IN 11 U.S.C. § 522(b)(3)(c).

Detailed Description |

|

Value |

|

|

|

|

|

|

10.COLLEGE SAVINGS PLANS QUALIFIED UNDER SECTION 529 OF THE INTERNAL REVENUE CODE.

(NCGS

Detailed Description |

|

Value |

|

|

|

|

|

|

11.RETIREMENT BENEFITS UNDER A RETIREMENT PLAN OF OTHER STATE AND GOVERNMENTAL UNITS OF OTHER STATES, TO THE EXTEND THOSE BENEFITS ARE EXEMPT UNDER THE LAWS OF THAT STATE OR GOVERNMENTAL UNIT. (NCGS

Description:

__________________________________________________________________________________

12.ALIMONY, SUPPORT, SEPARATION MAINTENANCE AND CHILD SUPPORT. (NCGS

91C (09/13)

Description:

__________________________________________________________________________________

13.ANY OTHER REAL OR PERSONAL PROPERTY WHICH DEBTOR DESIRES TO CLAIM AS EXEMPT THAT HAS NOT PREVIOUSLY BEEN CLAIMED ABOVE. (NCGS

|

Market |

|

|

Net |

Description |

Value |

Lien Holder(s) |

Amt. Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

______________________ |

___________ |

____________________ |

_________ |

_______ |

(a) Total Net Value of property claimed in paragraph 13. |

|

|

|

$ |

(b) Total amount available from paragraph 1(b). |

$ |

|

|

|

(c) Less amounts from paragraph 1(b) which were |

|

|

|

|

Used in the following paragraphs: |

|

|

|

|

Paragraph 3(b) |

$ |

|

|

|

Paragraph 4(b) |

$ |

|

|

|

Paragraph 5(c) |

$ |

|

|

|

Net Balance Available from paragraph 1(b) |

$ |

|||

|

Total Net Exemption |

$ |

||

14.OTHER EXEMPTIONS CLAIMED UNDER THE LAWS OF THE STATE OF NORTH CAROLINA:

Aid to the Aged, Disabled and Families with Dependent Children, NCGS

Yearly Allowance for Surviving Spouse, NCGS

North Carolina Local Government Employees Retirement Benefits, NCGS

Workers Compensation Benefits, NCGS

Unemployment Benefits, so long as not commingled and except for debts for necessities purchased while unemployed, NCGS

Group Insurance Proceeds, NCGS

Partnership Property, except on a claim against the partnership, NCGS

Other |

|

TOTAL VALUE OF PROPERTY CLAIMED AS EXEMPT |

$ |

15.EXEMPTIONS CLAIMED UNDER

Foreign Service Retirement and Disability Payments, 22 U.S.C. ' 1104 Social Security Benefits, 42 U.S.C. ' 407

Injury of Death Compensation Payments from War Risk Hazards, 42 U.S.C. ' 601 Wages of Fishermen, Seamen and Apprentices, 46 U.S.C. ' 601

Civil Service Retirement Benefits, 5 U.S.C. '' 729, 2265

Longshoremen and Harbor Workers Compensation Act Death and Disability Benefits, 33 U.S.C. ' 916

Railroad Retirement Act Annuities and Pensions 45 U.S.C. ' 228(L) Veterans Benefits, 45 U.S.C. ' 352(E)

Special Pension Paid to Winners of Congressional Medal of Honor, 38 U.S.C. ' 3101 Federal Homestead Lands, on Debts Contracted Before the Issuance of the Patent,

43 U.S.C. ' 175

Other |

|

TOTAL VALUE OF PROPERTY CLAIMED AS EXEMPT |

$ |

91C (09/13)

16.RECENT PURCHASES

The exemptions provided in NCGS

List tangible personal property purchased by the debtor less than 90 days preceding the filing of the bankruptcy petition:

|

Market |

|

|

Net |

Description |

Value |

Lien Holder(s) |

Amt. Lien |

Value |

______________________ |

___________ |

____________________ |

_________ |

_______ |

______________________ |

___________ |

____________________ |

_________ |

_______ |

DATE:

Debtor

| Fact | Detail |

|---|---|

| Form Identifier | 91C (09/13) |

| Court | United States Bankruptcy Court Middle District of North Carolina |

| Purpose | Debtor's Claim for Property Exemptions |

| Governing Laws | 11 U.S.C. '522(b)(3)(A), (B), and (C), Laws of the State of North Carolina, and non-bankruptcy federal law |

| Exemption for Residence or Burial Plot | NCGS 1C-1601(a)(1), with specific value limitations |

| Motor Vehicle Exemption | Limited to one vehicle under NCGS 1C-1601(a)(3) with a net value not to exceed $3,500 |

| Exemption Categories | Includes tools of trade, personal household property, life insurance, prescribed health aids, compensation rights, retirement plans, and more |

| Non-Bankruptcy Federal Exemptions Included | Includes various sources such as Social Security benefits, Veterans benefits, and others |

| Recent Purchases Clause | Addressed under NCGS 1C-1601(a)(2), (3), (4), and (5) for property purchased less than 90 days before bankruptcy filing |

After deciding to fill out the North Carolina 91C form for claiming property exemptions, it's essential to proceed systematically. This form is crucial for individuals navigating through bankruptcy as it allows them to protect certain assets by declaring them exempt from creditors' claims. To ensure accuracy and compliance, follow these detailed steps to complete the form correctly.

Upon completing the form, review it thoroughly to ensure all information is accurate and complete. This document will play a significant role in your bankruptcy proceedings by protecting vital assets from being used to pay off creditors. Once satisfied with the information provided, submit the form to the appropriate party as directed in your bankruptcy case instructions.

The North Carolina 91C form, utilized within the United States Bankruptcy Court for the Middle District of North Carolina, is a document filed by debtors to claim property exemptions under various laws, including section 522(b)(3)(A), (B), and (C) of the United States Bankruptcy Code, the laws of the State of North Carolina, and non-bankruptcy federal law. This form allows debtors to identify and claim specific properties as exempt, meaning they are protected from being seized or sold off to pay debts during bankruptcy proceedings.

Debtors undergoing bankruptcy proceedings in the Middle District of North Carolina need to file the 91C form if they wish to claim exemptions for their property. This form is a critical step for individuals seeking to protect certain assets from creditors during the bankruptcy process.

Various types of property can be exempted using the 91C form, including but not limited to:

The exemption amount for each type of property is determined by specific North Carolina General Statutes (NCGS) and federal laws. The form lists various categories of assets along with corresponding statutory exemption limits. For example, the exemption limit for a motor vehicle is $3,500, while personal property used for household purposes has a basic exemption limit of $5,000, with additional amounts for dependents.

Yes, in certain cases a debtor may claim an amount of interest that exceeds the statutory exemption limit on the property used as a residence, up to $125,000, provided specific conditions are met. However, for most other types of property, the exemption limits prescribed by the NCGS and federal laws are fixed and cannot be exceeded.

After filing the 91C form and successfully claiming property as exempt, the exempted assets are protected from being taken by creditors to satisfy debts. This means the debtor retains ownership of the property throughout and after the bankruptcy process, subject to the conditions and limits set by law.

Amendments to the 91C form can be made after it's initially filed, but this is subject to the approval of the bankruptcy court. Debtors may need to provide a valid reason for the amendment, such as correcting an oversight or responding to changes in their financial situation or in the valuation of their property.

The 91C form should be filed promptly once bankruptcy proceedings begin. While specific deadlines can vary depending on the case, failing to file the necessary paperwork in a timely manner may result in the loss of the opportunity to claim certain exemptions. It is advisable to consult with a bankruptcy attorney to ensure all filings are done correctly and within the required timeframes.

Debtors seeking assistance with the 91C form can find more information through the United States Bankruptcy Court for the Middle District of North Carolina's official website or by consulting a qualified bankruptcy attorney. Legal aid organizations may also offer assistance to those who qualify based on income or other criteria.

When navigating the complexities of the North Carolina 91C form, it's easy to make mistakes that can impact your bankruptcy case. Below are seven common errors to avoid:

Failing to check the box if the debtor claims an interest exceeding $125,000 in a primary residence. This oversight can lead to a misrepresentation of your exemptions.

Selecting the wrong exemption amount for real or personal property used as a residence or burial plot. The choice between the $35,000 and $60,000 exemptions requires careful consideration of your marital status and age, among other factors.

Incorrectly listing the market value and amounts of liens against property. Accurate calculations are crucial to determine the net value and exemption you're entitled to claim.

Overlooking the option to carry forward an unused portion of the homestead exemption. Up to $5,000 of any unused exemption can significantly impact your ability to exempt other properties.

Misreporting the value of a motor vehicle. Remember, only one vehicle is allowed under this exemption, and its net value cannot exceed $3,500 after liens.

Underestimating the value of personal property used for household or personal purposes. The total value includes items for you and your dependents, with specific limits.

Not considering all available exemptions under state and non-bankruptcy federal law. Many people miss out on valuable exemptions because they're unaware of their options.

Attention to detail and a thorough understanding of the exemptions available under the North Carolina 91C form can help protect as much of your property as possible during bankruptcy proceedings. Consultation with a legal professional can provide clarity and ensure that you make the most out of the exemptions you're entitled to.

Filing for bankruptcy in North Carolina involves more than just completing the North Carolina 91C form. This crucial document outlines the debtor's claim for property exemptions under both federal and state laws. However, to navigate through the bankruptcy process efficiently and effectively, several other forms and documents are often required, each serving a unique purpose in supporting your case.

Together, these forms and documents paint a full picture of the debtor's financial situation, laying the groundwork for a successful bankruptcy filing. Given the complexity and nuances of bankruptcy law, understanding each document’s role can significantly impact the outcome of a case. Therefore, it's advisable to approach these documents with thorough attention to detail, ensuring that every piece of information presented is accurate and complete to navigate the bankruptcy process smoothly.

The North Carolina 91C form, used in bankruptcy cases, allows debtors to claim certain property as exempt, meaning it cannot be used to pay off debts. This form has counterparts in various states, each designed to protect debtors from losing everything to bankruptcy. The idea is to provide a balance between satisfying creditors and not leaving debtors destitute. One key document similar to the 91C is the Schedule C form used in bankruptcy filings across the United States. Like the 91C, Schedule C allows filers to list properties they deem exempt, under federal or state laws, ensuring individuals can retain essential assets for a fresh start post-bankruptcy.

Homestead declaration forms found in many states resemble the real or personal property exemption sections of the 91C form. These declarations protect a portion of a debtor's home or property from being seized by creditors, under state-specific laws. North Carolina's 91C provision for exempting a debtor's residence or burial plot parallels these homestead protections, ensuring individuals don't lose their homes over financial distress.

Vehicle exemption forms, similar to the motor vehicle exemption section of the 91C, exist in various jurisdictions, allowing individuals to exempt a portion of their vehicle's value from bankruptcy estates. This acknowledges the essential role of transportation in seeking employment or attending to daily chores, making it a key aspect of exemptions aimed at supporting debtors' rehabilitation and reintegration into economic life.

Tools of the trade exemption documents are akin to the 91C's section permitting the exemption of work-related tools, books, and implements. These forms cater to professionals and tradespeople who require specific tools to earn a living. By allowing these items to be exempt from bankruptcy proceedings, the law ensures that debtors can continue their professions or trades post-bankruptcy, crucial for their financial recovery.

Personal property exemption forms, paralleling the 91C's section on household and personal items, enable debtors to protect everyday living essentials from seizure. Recognizing the personal and practical value of such items, these forms ensure debtors retain a basic standard of living, which is fundamental to their dignity and ability to rebound from financial setbacks.

Insurance benefits exemption documents, as reflected in the 91C form's section on life insurance, allow certain insurance policies and their proceeds to be shielded from creditors. This protects a debtor's investment in life insurance, ensuring that the financial safety net intended for survivors remains intact even when the policyholder faces bankruptcy.

Health aids exemption forms mirror the 91C's provisions on professionally prescribed health aids for debtors or their dependents. By exempting such items, the law acknowledges the paramount importance of health and well-being, ensuring that bankruptcy does not compromise the medical needs of the debtor or their family.

Wage exemption forms, though not directly mirrored in the 91C, relate to its purpose of allowing individuals to maintain their livelihood. Certain states permit a portion of a debtor's wages to be exempt from garnishment, ensuring individuals have the necessary funds for basic needs, similar to how the 91C protects essential property.

Retirement account exemption documents, akin to the 91C’s section on retirement plans, shield retirement savings from creditors. Given the essence of retirement savings for an individual's future, these exemptions ensure that a debtor's financial insecurity today does not jeopardize their financial security in retirement.

Lastly, education savings accounts, similar to the 91C's provision on college savings plans, can be exempted to secure a child's educational future. By protecting these funds, the law prioritizes the long-term educational opportunities for children of debtors, reflecting a societal commitment to education and future generations.

When filling out the North Carolina 91C form, it's important to pay close attention to both the instructions and the details you're providing. Here are some dos and don'ts to keep in mind:

Do:

Don't:

When individuals confront the complexity of bankruptcy, the North Carolina 91C form emerges as a critical document. However, misconceptions about this form can add to the confusion and potentially mislead those aiming to navigate through their financial difficulties effectively. Here, we aim to clarify six common misunderstandings to aid in a more accurate interpretation and utilization of the form.

One form fits all situations: The 91C form is designed specifically for use within the United States Bankruptcy Court for the Middle District of North Carolina. It's tailored to comply with both federal and North Carolina state laws regarding bankruptcy exemptions. Therefore, assuming that this form or its exemptions apply universally across all states can lead to incorrect claims or filings.

Unlimited exemption amounts: While the form provides a framework for claiming various property exemptions, these are not limitless. For example, exemptions for personal or real property used as a residence, motor vehicles, and tools of the trade have explicit caps on the amount that can be declared exempt from bankruptcy proceedings.

All personal property is covered: Misinterpretation often occurs around personal property exemptions. Although the form allows for exemptions on household and personal items needed by the debtor or dependents, there's a combined cap, and not all personal items may qualify for exemption. Understanding the specific criteria and limits is crucial.

Recent purchases are automatically exempt: There's a misconception that all personal property, irrespective of when it was obtained, can be claimed as exempt. However, the form delineates that property purchased within 90 days before filing for bankruptcy might not qualify for exemption, reflecting an effort to prevent last-minute acquisition of assets with the intention of declaring them exempt.

Exemptions don't require documentation: Completing the 91C form requires detailed information about each item or asset a debtor wishes to claim as exempt. This includes descriptions, market value, and existing liens against them. Simply listing items without substantiating their status and value can lead to challenges or disqualification of exemptions.

Claiming exemptions is optional and without consequence: Some might wrongly believe that failing to claim exemptions or deciding not to do so has little impact on the bankruptcy process. In reality, exemptions play a crucial role in determining what a debtor can retain through bankruptcy. Not claiming or improperly claiming exemptions could result in losing assets that could have been protected.

Understanding and accurately completing the North Carolina 91C form is a pivotal step for those pursuing bankruptcy relief under the protection of the law. Misconceptions can not only misguide but also potentially jeopardize one's financial recovery process. It's advisable for debtors to seek knowledgeable guidance or legal counsel to navigate these complexities effectively.

Filling out the North Carolina 91C form requires understanding its purpose and the details necessary to properly declare your property exemptions during bankruptcy proceedings. The form is structured to help individuals navigate through bankruptcy while retaining certain essential assets under both federal and state exemption laws. Here are key takeaways:

This form not only provides a structured pathway for determining what a debtor can retain during bankruptcy but also reflects an intersection of federal and state efforts to balance the rights and obligations of debtors with the interests of creditors.

D400 Form - A means for pregnant NCSU staff to discuss and arrange for additional radiation safety measures.

Nc Hauling Permits - Companies or individuals must specify the type of load, such as construction equipment or specific beam lengths, to assess the permit requirements accurately.

Workers Compensation North Carolina - Official document for notifying alterations in compensation benefits under the North Carolina Workers' Compensation Act.