Blank D 422 North Carolina PDF Form

Blank D 422 North Carolina PDF Form

Navigating the complexities of tax compliance represents a significant aspect of financial management, especially for residents familiarizing themselves with the nuances of local tax obligations. The D-422 North Carolina form, revised in December 1998, emerges as a critical document for those assessing their stance on the underpayment of estimated taxes. Particularly relevant to individuals who anticipate the potential for owing a penalty due to underestimations, this document guides through the determination of the required annual payment and the meticulous process of penalty calculation, accommodating two distinct methodologies— the Short Method and the Regular Method. The form's instructions delineate the eligibility criteria for each approach, offering a streamlined process for taxpayers who adhered to payment deadlines with uniformity, and a more detailed procedure for those whose payments deviate from such regularity. Notably, special provisions are outlined for farmers and fishermen, acknowledging the unique temporal nature of their income and consequent tax liabilities. Moreover, the form caters to varying income scenarios, providing mechanisms to minimize penalty amounts through the Annualized Income Installment Worksheet. Such a comprehensive framework underscores the importance of understanding and adhering to structured payment schedules, while also offering flexibility and relief for particular circumstances and taxpayer needs.

(Rev. |

|

1998 |

Form |

NORTH CAROLINA DEPARTMENT OF REVENUE |

|

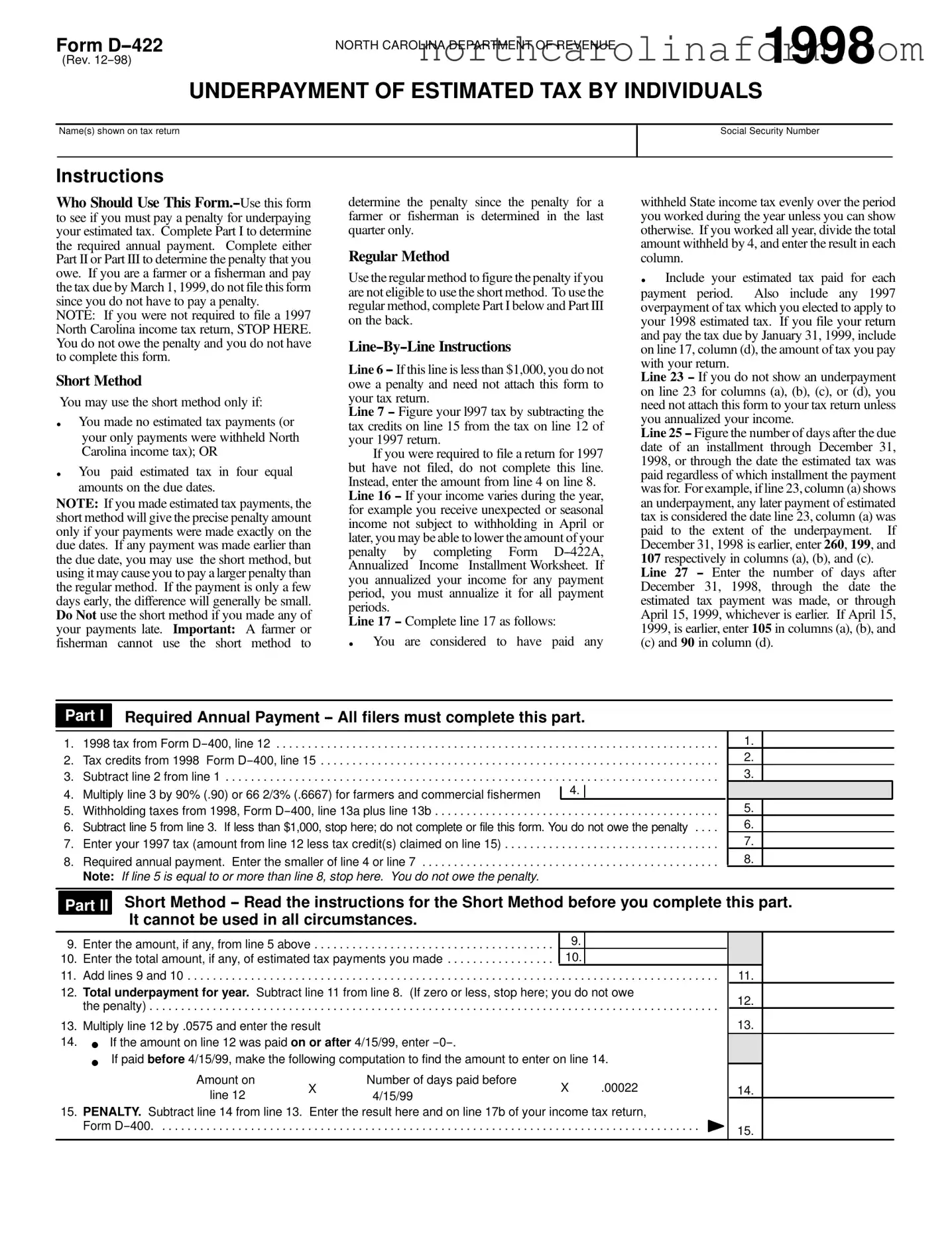

UNDERPAYMENT OF ESTIMATED TAX BY INDIVIDUALS

Name(s) shown on tax return

Social Security Number

Instructions

Who Should Use This

NOTE: If you were not required to file a 1997 North Carolina income tax return, STOP HERE. You do not owe the penalty and you do not have to complete this form.

Short Method

You may use the short method only if:

. You made no estimated tax payments (or your only payments were withheld North Carolina income tax); OR

. You paid estimated tax in four equal amounts on the due dates.

NOTE: If you made estimated tax payments, the short method will give the precise penalty amount only if your payments were made exactly on the due dates. If any payment was made earlier than the due date, you may use the short method, but using it may cause you to pay a larger penalty than the regular method. If the payment is only a few days early, the difference will generally be small. Do Not use the short method if you made any of your payments late. Important: A farmer or fisherman cannot use the short method to

determine the penalty since the penalty for a farmer or fisherman is determined in the last quarter only.

Regular Method

Use the regular method to figure the penalty if you are not eligible to use the short method. To use the regular method, complete Part I below and Part III on the back.

Line 6

Line 7

If you were required to file a return for 1997 but have not filed, do not complete this line. Instead, enter the amount from line 4 on line 8.

Line 16

Line 17

. You are considered to have paid any

withheld State income tax evenly over the period you worked during the year unless you can show otherwise. If you worked all year, divide the total amount withheld by 4, and enter the result in each column.

. Include your estimated tax paid for each

payment period. Also include any 1997 overpayment of tax which you elected to apply to your 1998 estimated tax. If you file your return and pay the tax due by January 31, 1999, include on line 17, column (d), the amount of tax you pay with your return.

Line 23

Line 25

Line 27

(c) and 90 in column (d).

Part I

Required Annual Payment

1. |

1998 tax from Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

2. |

Tax credits from 1998 Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

3. |

Subtract line 2 from line 1 |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

4. |

Multiply line 3 by 90% (.90) or 66 2/3% (.6667) for farmers and commercial fishermen |

|

4. |

|

|

|

|||

5. |

Withholding taxes from 1998, Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

6. |

Subtract line 5 from line 3. If less than $1,000, stop here; do not complete or file this form. You do not owe the penalty . . . . |

|||

7. |

Enter your 1997 tax (amount from line 12 less tax credit(s) claimed on line 15) |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

8. |

Required annual payment. Enter the smaller of line 4 or line 7 |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

|

Note: If line 5 is equal to or more than line 8, stop here. You do not owe the penalty. |

|

|

|

1.

2.

3.

5.

6.

7.

8.

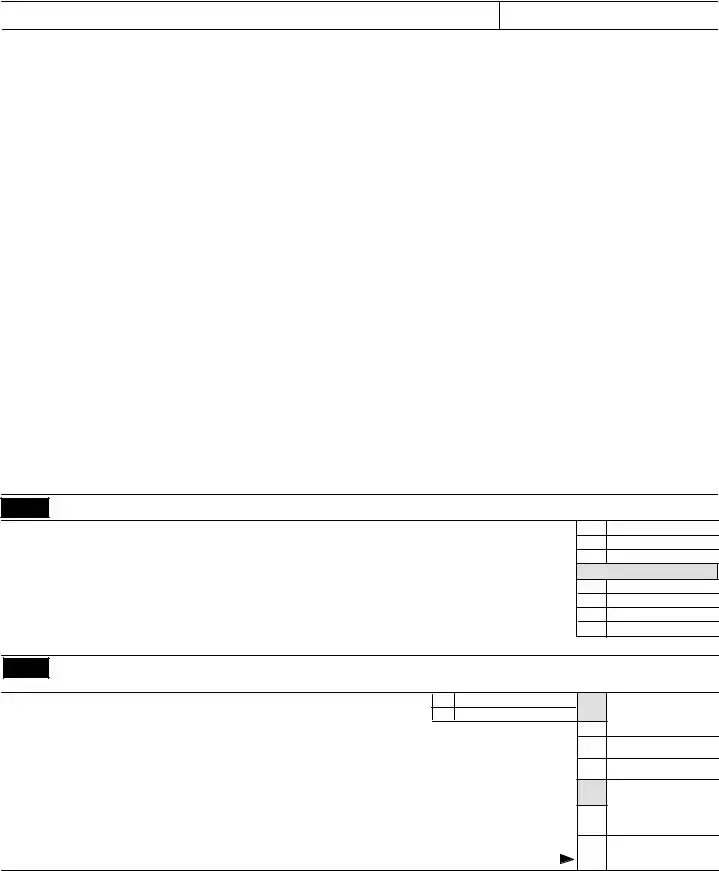

Part II

Short Method

9. |

Enter the amount, if any, from line 5 above |

9. |

|

|

|||

10. |

Enter the total amount, if any, of estimated tax payments you made |

10. |

|

|

|||

11. |

Add lines 9 and 10 |

11. |

|||||

12. |

Total underpayment for year. Subtract line 11 from line 8. (If zero or less, stop here; you do not owe |

12. |

|||||

|

the penalty) |

||||||

|

|

||||||

13. |

Multiply line 12 by .0575 and enter the result |

|

|

|

13. |

||

14. |

. |

If the amount on line 12 was paid on or after 4/15/99, enter |

|

|

|

||

|

. |

If paid before 4/15/99, make the following computation to find the amount to enter on line 14. |

|

||||

|

Amount on |

|

Number of days paid before |

|

|

|

|

|

|

X |

X |

.00022 |

14. |

||

|

|

line 12 |

4/15/99 |

||||

|

|

|

|

|

|

||

15. |

PENALTY. Subtract line 14 from line 13. |

Enter the result here and on line 17b of your income tax return, |

|

||||

|

Form |

15. |

|||||

|

|

|

|

|

|

|

|

Form

Page 2

|

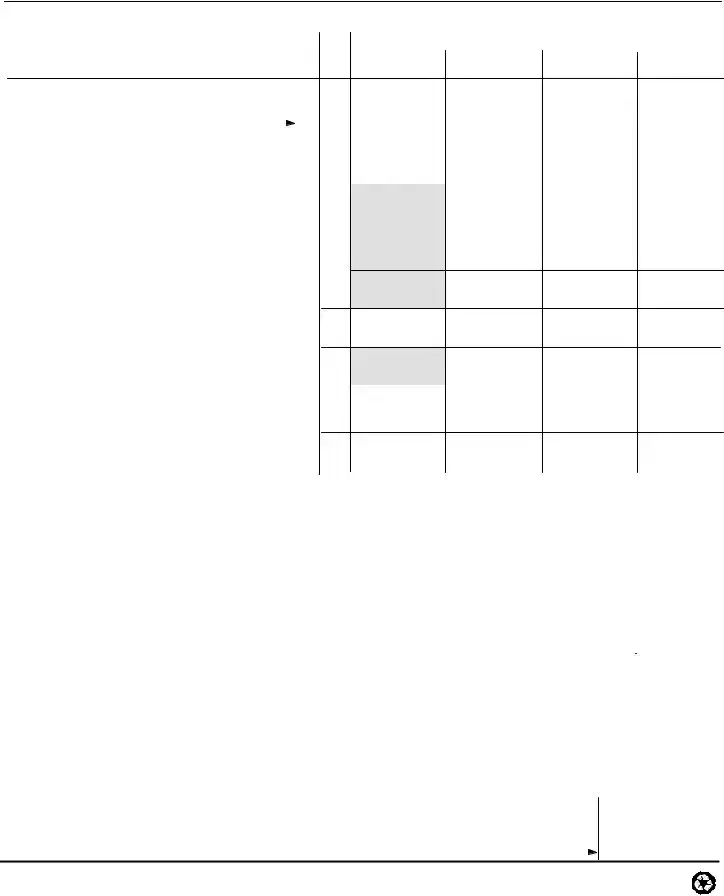

Part III |

Regular Method |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section A |

|

|

Payment Due Dates |

|

||

|

|

(a) |

(b) |

(c) |

(d) |

||

|

|

|

|

4/15/98 |

6/15/98 |

9/15/98 |

1/15/99 |

16.Divide line 8 by 4 and enter the result in each column. Exception: If you use the annualized income

|

ment method, complete Form |

|

16. |

|

|

||||

17. |

Income Installment Worksheet) and check this box. |

|

|

|

|

|

|||

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

Estimated tax paid and tax withheld. For column (a) only, |

|

|

|

|

|

||||

|

|

|

|

|

|

||||

|

enter the amount from line 17 on line 21. (If line 17 is |

|

|

|

|

|

|||

|

equal to or more than line 16 for each payment period, |

17. |

|

|

|||||

|

. . . .stop here; you do not owe the penalty.) |

|

|

||||||

|

|

|

|||||||

|

Complete lines 18 through 24 of one column before |

|

|

|

|

|

|||

|

going to the next column. |

|

|

|

|

|

|||

18. |

Enter amount, if any, from line 24 of previous colum . . . . |

18. |

|

|

|||||

|

|

19. |

|

|

|||||

19. |

Add lines 17 and 18 |

|

|

||||||

20. |

Add amounts on lines 22 and 23 of the previous column |

|

|

and enter the result |

20. |

21.Subtract line 20 from line 19 and enter the result. If zero

or less, enter zero. (For column (a) only, enter the |

|

amount from line 17) |

21. |

22.Remaining underpayment from previous period. If the

amount on line 21 is |

||

and enter the result. Otherwise, enter |

. . . . 22. |

|

23. Underpayment. If line 16 is larger than or equal |

to |

|

line 21, subtract line 21 from line 16 and enter the |

||

result. Enter 0 on line 18 of the next column and go to |

||

line 19. Otherwise, go to line 24 |

. . . . 23. |

|

24.Overpayment. If line 21 is larger than line 16, subtract

|

|

line 16 from line 21 and enter the result. Then go to |

|

|

|

|

|

|

|||||

|

|

line 18 of next column. . |

. . . . . . . . . . . . . . . . . . . . |

. . . . |

. . . . 24. |

|

|

|

|

||||

|

Section B Figure the Penalty (Complete lines 25 through 28 of one column before going to the next |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

April 15, 1998 December 31, 1998 |

|

|

|

|

|

|

|

||||

|

|

|

|

|

4/15/98 |

6/15/98 |

9/15/98 |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

25. Number of days after the date shown above line 25 through |

|

Days: |

Days: |

Days: |

|

|||||||

|

|

the date the amount on line 23 was paid or |

12/31/98, |

|

|

|

|

|

|||||

|

|

whichever is earlier. |

. . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . |

25. |

|

|

|

|

|||

|

26. |

Underpayment |

X |

|

Number of days |

X |

.09 |

|

|

|

|

|

|

|

|

on line 23 |

|

on line 25 |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(see instructions) |

|

365 |

|

|

|

26. |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

January 1, 1999 |

April 15, 1999 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

12/31/98 |

12/31/98 |

12/31/98 |

1/15/99 |

|||||

|

|

|

|

|

|

|

|

|

|

||||

|

27. Number of days after the date shown above line 27 through |

|

Days: |

Days: |

Days: |

Days: |

|||||||

|

|

the date the amount on line 23 was paid or |

4/15/99, |

|

|

|

|

|

|||||

|

|

whichever is earlier. |

. . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . |

27. |

|

|

|

|

|||

|

28. |

Underpayment |

X |

|

Number of days |

X |

.08 |

|

|

|

|

|

|

|

|

on line 23 |

|

on line 27 |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(see instructions) |

|

365 |

|

|

|

28. |

$ |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

|

|||||

29.Penalty (add amounts on line 26 and 28). Enter here and on line 17b of your individual income tax return,

Form

29.

| Fact Name | Description |

|---|---|

| Form Purpose | The Form D-422 is utilized to determine if an individual owes a penalty for underpaying their estimated tax in North Carolina. |

| Eligibility for Short Method | The short method for calculating the penalty is available only if no estimated tax payments were made, or if estimated tax was paid in four equal amounts on the due dates. |

| Special Consideration for Farmers and Fishermen | Farmers and fishermen who pay their due tax by March 1, 1999, do not need to file this form as they are exempt from the penalty. |

| Governing Law | This form is regulated under the authority of the North Carolina Department of Revenue, adhering to state-specific tax laws and regulations. |

Understanding how to properly complete the D-422 North Carolina form is vital for individuals concerned about underpayment of their estimated tax. This document aids in the calculation of any possible penalties due to underpayment. To ensure accuracy and avoid potential fines, follow the steps meticulously. Remember, if you are a farmer or fisherperson with your tax due paid by March 1, 1999, this form and penalty do not apply. Additionally, if you didn't need to file a North Carolina income tax return for the previous year, you can forego this form.

Accurately following these steps ensures compliance with North Carolina's tax regulations and minimizes the risk of unnecessary penalties. For further clarification on specific line items or more unique tax situations, consulting the detailed instructions provided by the North Carolina Department of Revenue or a tax professional may prove beneficial.

The D-422 form, issued by the North Carolina Department of Revenue, is designed to help individuals determine whether they owe a penalty for underpaying their estimated tax. It is particularly relevant for those who have not met the required annual payment through withholdings or quarterly estimated tax payments. The form includes calculations to ascertain the precise penalty amount owed, if applicable.

Individuals who have underpaid their estimated tax in North Carolina should use the D-422 form to evaluate whether they are subject to a penalty. Notably, those who haven't had to file a North Carolina income tax return for the previous year (such as the sample's reference to not needing to file if one didn't have to file a 1997 tax return) or those meeting specific criteria as farmers or fishermen, with provisions allowing for delayed payment without penalty, are exempt from filing this form.

The short method for calculating the penalty on the D-422 form is limited to individuals who either had no estimated tax payments (except for withholdings) or made equal estimated tax payments on the four due dates. This method simplifies the computation but may result in a higher penalty if payments were made before the due dates. It's not suitable for individuals who have made late payments or for farmers and fishermen, who have their penalties calculated in the last quarter only.

The regular method for calculating the underpayment penalty is more comprehensive than the short method and is used when the latter's conditions are not met. It involves a detailed line-by-line calculation that considers the exact payment dates and amounts throughout the year. This method is especially useful for accounting for varied income or late payments, potentially resulting in a more accurate—and often lower—penalty calculation.

If you discover that you've overpaid your estimated tax after completing the form D-422, this overpayment may be applied to your next tax year's estimated tax or refunded, depending on your preference. The form itself does not cover the procedure for addressing overpayments, hence you should consult the North Carolina Department of Revenue's guidelines or contact them directly for instructions on how to proceed.

Filing the D-422 form is not mandatory for all taxpayers. It is specifically designed for individuals who may have underpaid their estimated taxes and are trying to determine if they owe a penalty. If your withholdings or estimated payments equal or exceed the required annual payment, or if your tax liability is less than $1,000, you do not need to complete or file this form. Additionally, if you did not have to file a North Carolina tax return for the previous year, you're exempt from filing this form.

When filling out the Form D-422 for the North Carolina Department of Revenue, individuals often make mistakes that can lead to incorrect penalty calculations or processing delays. Recognizing and avoiding these errors can streamline the submission process and ensure accuracy in underpayment evaluations.

Not verifying eligibility before using the short method. The short method cannot be applied universally; it is limited to those who made no estimated tax payments or whose only payments were North Carolina income tax withholdings, and those who paid in four equal installments. Attempting to use this method without meeting these prerequisites can result in inaccuracies.

Using the short method despite making early or late payments. Since the accuracy of the short method hinges on payments being made precisely on the due dates, any deviation makes this method unsuitable and can lead to overestimated penalties.

Omitting the form when not owing a penalty. If no underpayment is shown on line 23 for any column, or if one's income is annualized, the form must still be attached unless specified conditions are met, creating a common oversight.

Incorrectly annualizing income or failing to do so for all payment periods. If income varies, accurately completing Form D-422A for each payment period is essential. Missteps here can erroneously impact the calculated penalty.

Misunderstanding the prepayment credit application. Taxpayers often err by inaccurately dividing their withheld taxes evenly throughout the year or by improperly accounting for applied 1997 overpayments against their 1998 estimated tax.

Skipping lines or sections that apply. Particularly in Part III, missing any steps in the regular method calculation—such as forgetting to carry over amounts from one column to the next—can significantly distort the penalty amount.

Erroneously calculating the number of days past due for installments and final payments. Correctly figuring the number of days from the due date of an installment (lines 25 and 27) ensures the penalty is calculated based on an accurate timeframe.

By diligently avoiding these points of confusion, filers can more accurately complete Form D-422 and avoid unnecessary penalties for the underpayment of estimated taxes.

When dealing with the intricacies of tax filings and potential penalties for underpayment of estimated taxes in North Carolina, it's paramount to have a comprehensive understanding of the forms and documents that can accompany Form D-422. This knowledge ensures that individuals can navigate their tax obligations more smoothly and avoid common errors that might lead to further penalties. Below, find a list of documents often used alongside Form D-422 and a brief description of each to guide you through the process.

Understanding and preparing the correct forms and documents alongside Form D-422 is essential for accurately calculating and potentially minimizing any underpayment penalties. By familiarizing yourself with these forms, you can better manage your tax obligations in North Carolina and ensure that you comply with all state tax laws. Should you find this process overwhelming, consulting with a tax professional may provide valuable guidance tailored to your specific financial situation.

The Form D-422 from North Carolina shares similarities with the IRS Form 2210, "Underpayment of Estimated Tax by Individuals, Estates, and Trusts." Both forms are designed for taxpayers who might not have paid enough in estimated taxes throughout the year, potentially incurring a penalty. They guide the taxpayer through calculations to determine whether they owe a penalty and, if so, how much. Each form takes into account the total tax expected to be owed, subtracts withholdings and credits, and divides the resulting number by specific dates to measure underpayment per period.

Another similar document is the IRS Form 1040-ES, "Estimated Tax for Individuals." This form is used for calculating and paying estimated taxes quarterly. Though the Form D-422 North Carolina and Form 1040-ES serve different functions—one for addressing underpayment penalties and the other for estimating and submitting future tax payments—they both revolve around the concept of paying taxes ahead of filing a return. Both forms cater to individuals, including specific groups like farmers and fishermen, emphasizing their tax responsibilities throughout the fiscal year.

The Form D-422A, specifically referenced within the D-422 instructions as the "Annualized Income Installment Worksheet," is closely related in its purpose and application. This form is used when income is not received evenly throughout the year, allowing taxpayers to calculate their estimated tax based on the actual period income was earned, which might lower the amount of the penalty by aligning tax payments more closely with cash flow. It directly supports the calculations required for D-422, allowing for a more precise penalty computation under irregular income circumstances.

The fourth form that bears resemblance to North Carolina's D-422 is the IRS Form 8801, "Credit for Prior Year Minimum Tax—Individuals, Estates, and Trusts." Although Form 8801 primarily deals with the minimum tax credit carryover to the next year, it shares with D-422 the conceptual framework of adjusting current year obligations based on prior payments or credits. Both forms target individuals and involve intricate calculations to ensure taxpayers' payments align with their tax responsibilities, allowing for adjustments based on previous fiscal activities.

Filling out the D-422 North Carolina form, a document designed for calculating underpayment of estimated tax by individuals, requires attention to detail and understanding of your tax situation. Here are some dos and don'ts to guide you through the process efficiently and accurately.

Dos:

Don'ts:

Understanding the D-422 North Carolina form can be challenging, leading to several common misconceptions. It's important to clarify these to ensure taxpayers fulfill their obligations accurately while avoiding unnecessary penalties.

This form is actually for individuals, including farmers and fishermen, who might underpay estimated tax, not just for business owners.

Only those who underpaid their estimated taxes need to complete it to determine if they owe a penalty.

The short method is not suitable for everyone. It's designed for individuals who made no estimated tax payments or paid in four equal amounts on due dates without deviation.

While it's true they cannot use the short method, farmers and fishermen who pay their due tax by March 1 following the tax year do not need to file this form or pay a penalty at all.

If you determine you don't owe a penalty, especially if your withholding taxes or estimated payments were enough, you don't need to attach the form to your return unless you annualize your income.

While getting professional advice is helpful, many individuals can navigate the form by carefully reading the instructions and understanding their own tax situation.

Penalties are specifically calculated based on underpayment amounts and their due dates. Slight variances, especially early payments, might not always result in a penalty.

Using Form D-422A, the Annualized Income Installment Worksheet, can allow taxpayers with varied income throughout the year to potentially reduce their penalty amount.

Understanding these aspects of the D-422 North Carolina form will help taxpayers avoid mistakes and unnecessary penalties. Always refer to the most current forms and instructions or seek professional advice for your specific tax situation.

Filling out the Form D-422 in North Carolina is required if you have underpaid your estimated tax for the year. This can seem like a daunting task, but understanding the key takeaways about the form can simplify the process. Here are 10 essential points to remember:

By keeping these pointers in mind, you can navigate the complexities of the Form D-422 with greater ease. Remember, the goal is to accurately report and remedy underpaid taxes to avoid unnecessary penalties, ensuring compliance with North Carolina's tax laws.

Nc19 - For establishing legal residency in North Carolina, this document necessitates declaration of domicile, supporting the claim with identifiable and residency information.

Notice of Right to Have Exemptions Designated - College savings plans recognized under Section 529 reflect the law’s recognition of the importance of educational planning and protection in financial distress scenarios.